Value creation is driving companies at every stage of their activity: from products to shareholders, including employees, the community, the environment, etc. The definition of Value creation is wide, and there is no consolidated literature about it: IndustryWeek has a whole section dedicated to value creation, and companies have their own view on this issue (see what value creation is according to BHP Billiton). The finance oriented approach is central. Corporate Finance from Brealey Myers & Marcus explains extensively own a project "creates value" for its owner/investor. Marketing Management, from Kotler and Keller, drags the concept of value creation all along the book. Strategy mainstream authors, and especially Michael Porter in his early papers (Competitive Advantage, 1985) prefer to define it using the concepts of competition and the company : Competitive advantage brings a sustainable added value vs. competition and the market. We believe this last definition symbolizes the most Revenue Management in its expected effects. Now, let's try to make our own generic and simple definition... there we go: Value creation is what brings a superior worth to a good or a service, on the perspective of a market. A good can be a company, a business unit, a product and it is to be viewed as positioned within an environment.

This is much discussed at every level of the corporate ladder. We believe this question is key for any RM implementation proposal. It is the role of the manager supporting the idea to bring some milestones along.

Evaluating the financial benefits of the implementation of an RM system in a company quickly proves to be complicated: We will dedicate an article to address this issue. Indeed, one can calculate an expected rate of return on an investment in software, machines or any tangible asset, where the material’s life span, cash flows and depreciation period are known a priori.

Here, we are talking about a change that is probably one of the most difficult to assess in a company: The impact of a new, structural management methodology, which is all but certain. The greater the expected returns are, the higher the risk is (yes... we have heard of this too!).

In this context, we think the concept of sustainability makes sense. Implementing a new management methodology is a long term project. To create value, Revenue Management first has to be seen as at the crossroads of strategy, finance and organizational theory; and secondly, optimization, demand forecast and customer behavior issues can be addressed. Building a transverse management methodology is a key prerequisite to generate organizational alignment and thus survive external events.

That is why we believe that a structured approach must be drawn: This article proposes a series of steps that would enlighten the feasibility study to support such a project. We therefore list a couple of steps or milestones that one should address when you coming with the idea of implementing Revenue Management.Step 1: Be aware that you may find yourself in a difficult position

Due to the influence of capital markets and private equity (and the related expected returns), business today (and probably yesterday as well) tends to focus on high yield and short term payback, The investor follows the risk paradigm and expects a proportional (or at least not contrary) return / yield. Therefore, everyone can understand that an investor, who is endowing in a firm in capital need to finance projects, is experiencing a risk, especially if the investment is about implementing a new, challenging management technique!

From our experience and readings (see Talluri and Van Ryzin, The Theory and Practice of Revenue Management), it takes quite some time to implement Revenue Management; even more if it is the first time: the needs have to be properly defined and studied, the organization’s rules, design and processes have to be reengineered to support RM. This means that, whatever the size of the business, a transition time is needed to get from the current to the targeted /optimal situation. An implementation can take several months up to several years.

This puts the manager in charge of the implementation in a difficult position: Investors could expect a “return” before the end of it, and will ask for an assessment of the first results of the newly implemented Revenue Management system. There is an inherent contradiction between a latent short-termism, and RM’s value creation which can take a bit of time before ramping up. This underlines the importance of sustainability.

Step 2: Build something called strategy, or at least, steer your organization.

First of all, Revenue Management is not a secret formula, enabling managers to create growth and value, forever (neither is value creation in general by the way). We think that such a sustainable value creation is the coordinate action of an organization with aligned people, methodologies, and stakeholders, willing to make the move and bring the company to the next level. This implies the alignment on long run business objectives and changes together with a short run operational management. Making this change be part of a strategic positioning would have more success and meet expectations (Michael Porter, What is strategy?, HBR Nov-Dec 1996) This whole is called “strategy”, and 2 companies out 3 lacks one – according to Henri Bouquin, Head of EMBA at Université Paris Dauphine, France in his book, Les fondamentaux du contrôle de gestion.)

Step 3: Try to assess a time period for Revenue Management.

Revenue Management has currently no standard usage time (even if depreciation is a calculation made by accounting…but everyone knows how accounting can sometimes not represent reality!). This is a key as depreciation is based on utilization rate or time of the asset Obsolescence, from to our point of view, can only come from superior optimization and forecasting algorithms within the competition, preventing your company to reach all your usual revenue streams. To our opinion, the prerequisite to the kick-off of a project, before convincing any investor and being misled thereafter, is assessing timing and usage time. For example, usage time could follow the life cycle of the product or the foreseeable market macro-changes. This way, you can adapt your management to your activity. Basic idea, but robust in a globalized world!

Step 4: Assess revenue increase and value creation.

This will be the full content of an article to be published later in May

Step 5: Keep in mind your (high) fixed costs and the levers to keep Revenue in a good shape

Rule of thumb: Revenue Management will create positive results as long as the activity of your company is not affected by uncontrollable exterior factors (we’re pretty smart on this blog J). If the activity slows down, revenues may lower, and it will be quite critical to determine whether or not Revenue Management is generating superior value for the company. In this context, value is strongly needed by the organization which has, more than ever, to sell to high yield customers. This is when capacity adjustments have to come into play. Indeed so far, one of the hypotheses was a fixed capacity. . However companies can to take advantage of that and must have rescue plan that assess the opportunity cost of shutting down part of the capacity.

Even if Revenue Management works well in capacity constrained industries, it doesn’t mean that it should not be changed if needed. This is easy for some businesses like hotels and cruise lines for example, where you can scale down more or less rapidly (selling part of your assets) and try to diminish slightly your costs. Unfortunately, other businesses (parking lots, restaurants for example) have more difficulties to reduce their capacities due to limited levers. Indeed it is not easy to fire employees in restaurants in Europe (ok… in France!) to wait fewer tables for example. Anyhow, shutting half of a car park or of a restaurant off would not have any effect on reducing the costs, as opportunity costs remain for the whole occupied space.

Step 6: Have a look around.

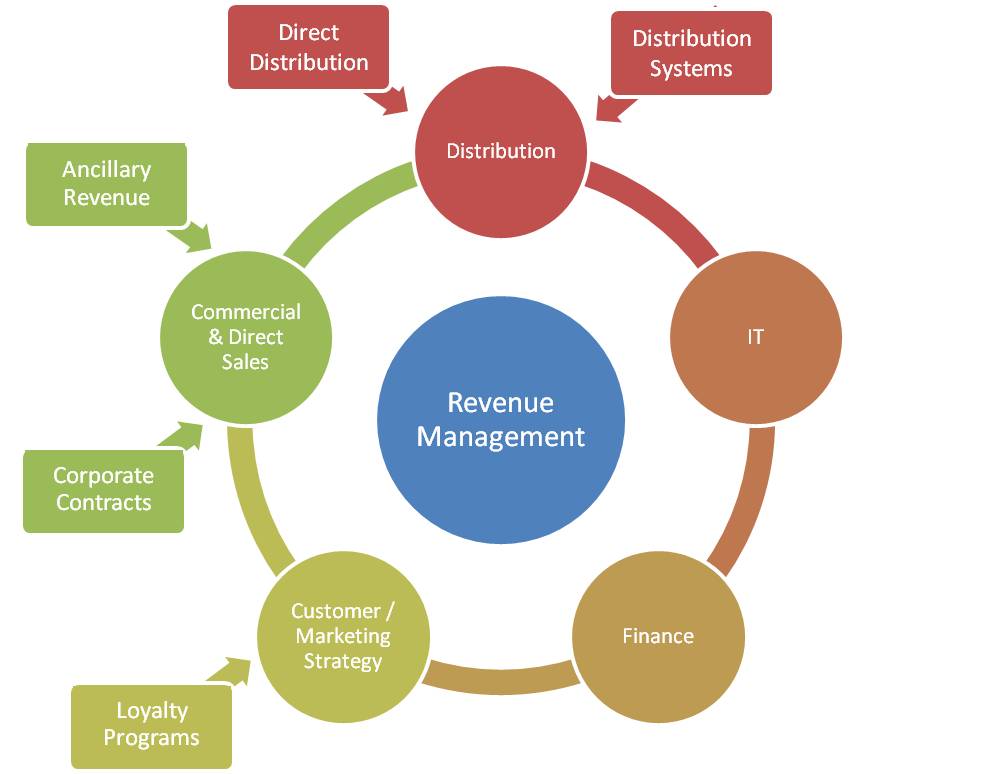

Of course, your market is not revolving around you and key players could look at each other and find ways to set up alliances, leaving you behind, alone. This has happened recently in the airline industry: the three main alliances (Star Alliance, Skyteam, Oneworld) created JV to form oligopoly in some transatlantic markets. This leaves remote players like SAS, Finnair with low market shares. Their only alternative to keep the statu quo is low prices. This is for sure a more of a strategic subject, but RM is a topic for alliances (Can we align our pricing policy? Who will manage the inventory?).Well, as an entrepreneur or a small business owner, you may not feel concerned with what is said above (even if we think that for every company size, there are markets and predators which will, as it is the goal of most corporations, grow!). We still believe distribution is a core lever for the successful implementation of revenue management. Indeed History shows that the first Global Distribution System (GDS) brought the first RM. Today, with the new techs, multi-channel distribution becomes easier than ever: Less complicated selling platforms have to be built (unlike GDS in the business travel industry. We are actively researching how could SMEs build their own distribution systems (based on a pool of companies, or one major) in order to secure the value chain and therefore increase overall chance to reach value creation expectations.

You might have noticed that in this article, value is not only addressed from a financial standpoint but also from an organizational and strategic point of view, as sustainability involves the whole company: This is our vision!

Despite the need for an overall view of business, numbers convince easily: We will go further in details for step 4 later this month.

See you soon!

Yoann and Julien

{kind=link}